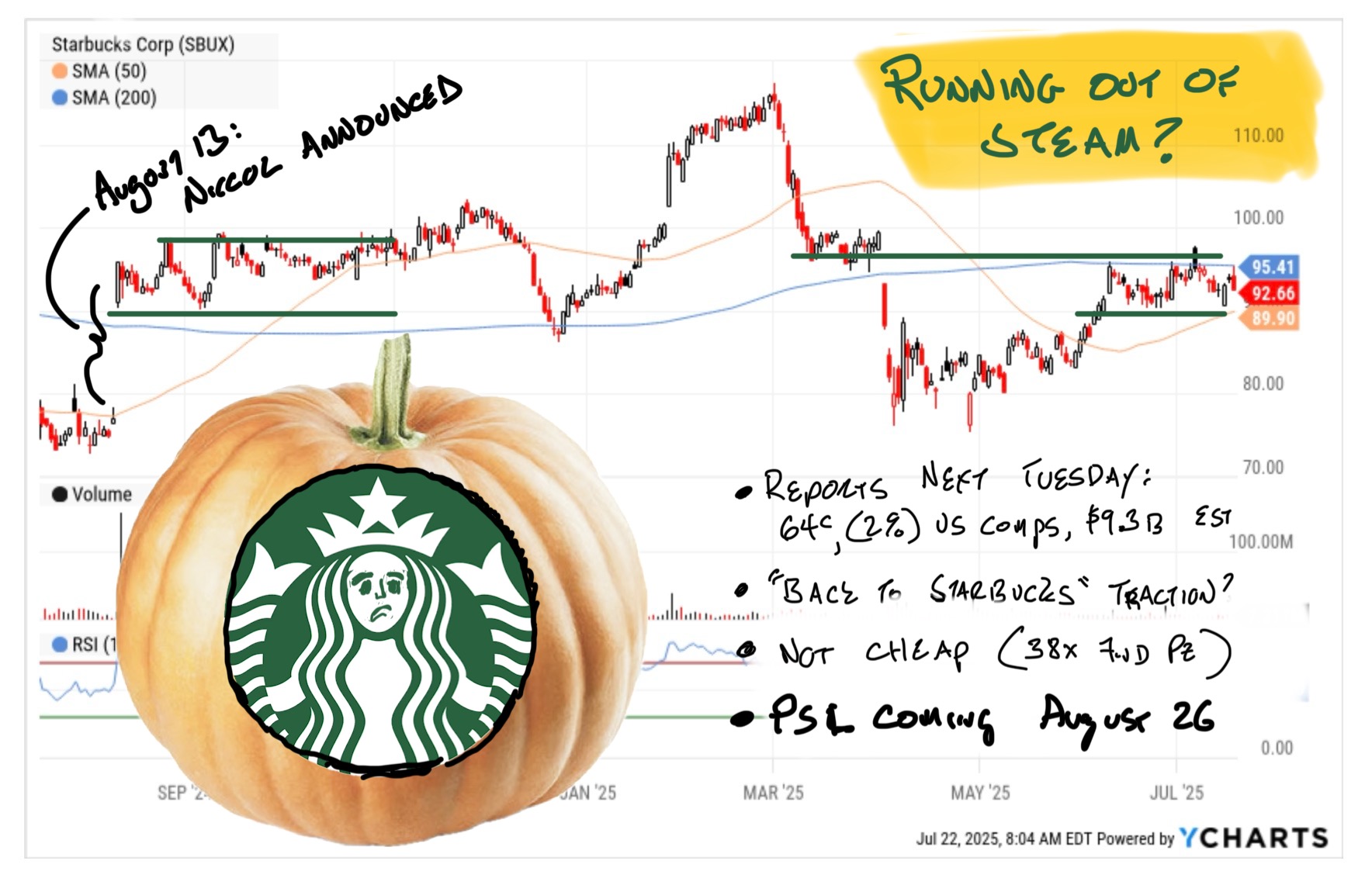

No one has been rooting for Starbucks harder than me, but the chain is running out of time. With the coffee giant set to report next week, and CEO Brian Niccol approaching his first anniversary since being announced as CEO it's time to review the Risk / Reward set-up for the stock.

Spoiler Alert: It's not great.

It's possible I was expecting too much from Brian Niccol when the former Chipotle CEO took the head job at Starbucks last August. Maybe I underestimated the amount of damage done by Niccol's predecessors, and how much time it would take to restore customer trust. Maybe energy drinks, ADHD drugs and Dutch Bros have combined to obviate America's need for a healthy 4 or 5 doses of coffee every day.

Whatever the reason, with the stock basically flat for 2025 and Starbucks set to report a week from today, this is a good time to ask myself just how committed I am to staying long $SBUX heading into Fall.

Low Expectations, High Multiple

While Niccol's efforts to recreate the "Starbucks as a Third Place" experience are gaining some traction it's not showing up in unit performance, let alone the price of $SBUX stock compared to rivals like Dutch Bros.

Starbucks is expected to report -2.2% comp unit sales at its 20,000 North American units next week despite an expected increase in average ticket next week. Unless Niccol and crew can pull an upset it will mark the 6th straight quarterly decline in comps for the chain, a distressing cold streak showing few signs of reversing.

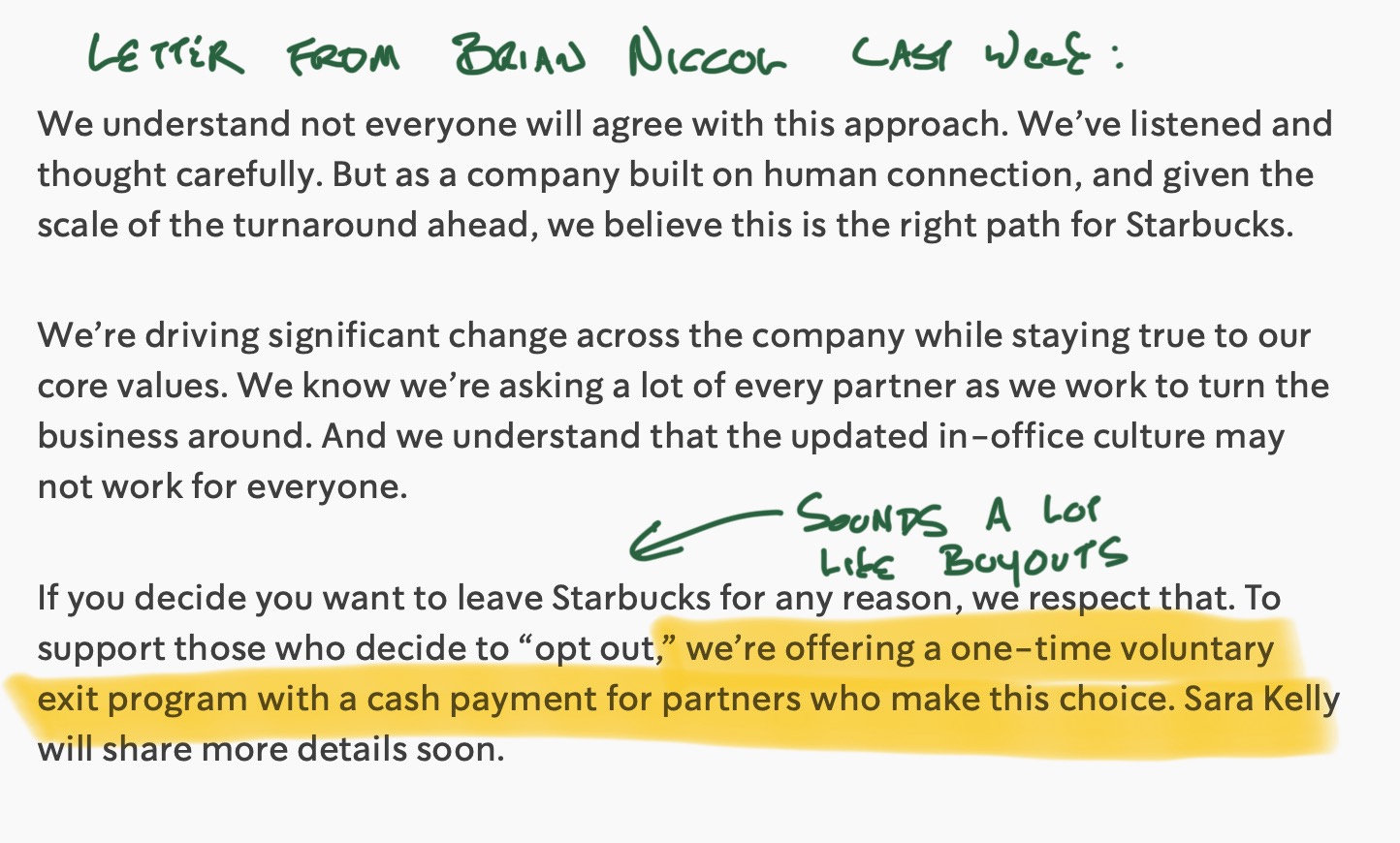

Also discouraging, nearly a year into his tenure Niccol still in cutting mode with Starbucks looking for a bidder in the moribound China segment and announcing a Return to In-Office-Work memo last week which sounded a lot like downsizing.

Too Expensive to be a Value Play

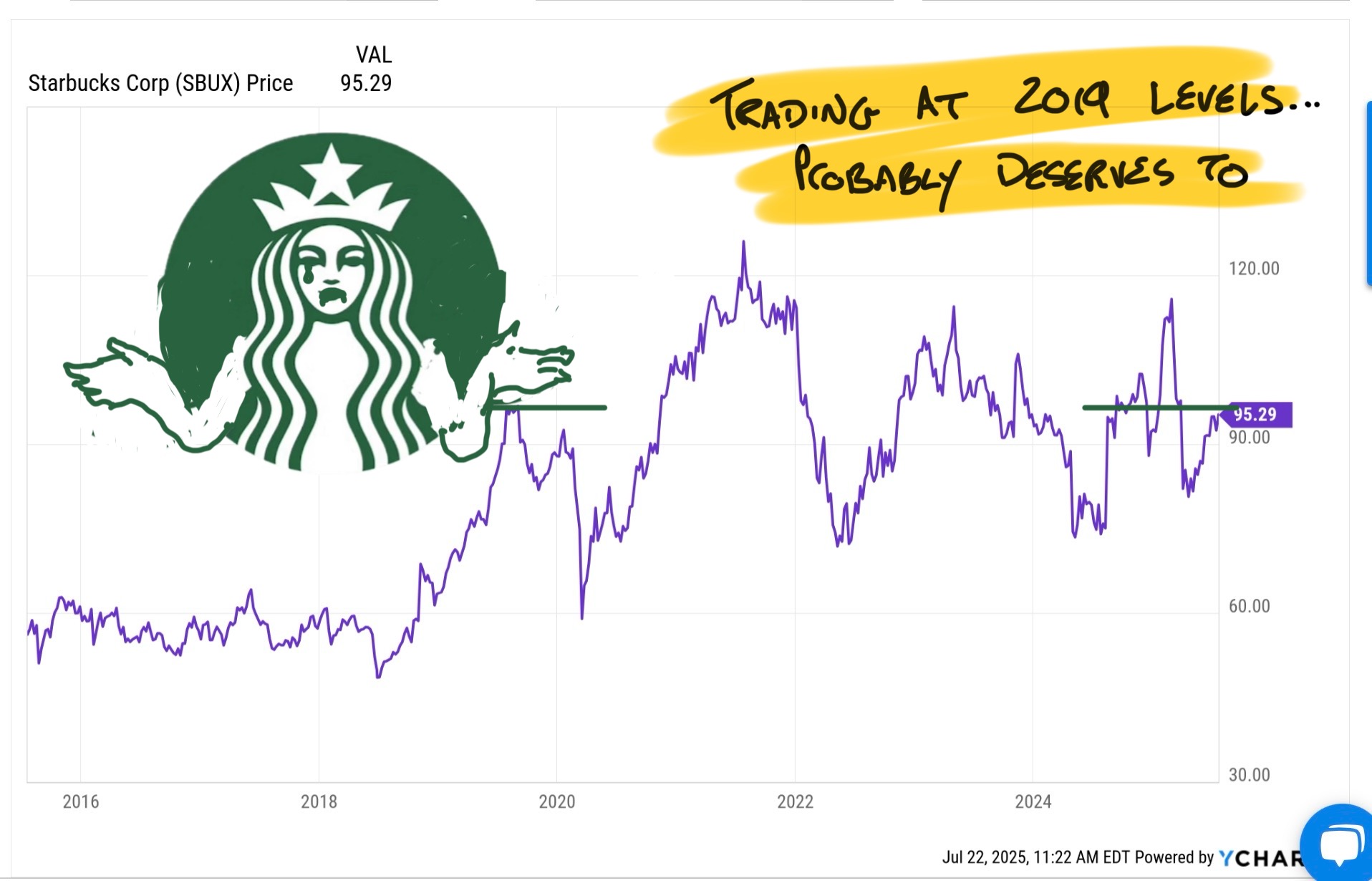

If $SBUX were a cheap stock or still in growth mode, it would be much easier to stay long and let Niccol cook. It's not that he's making bad strategic decisions; it's that it's going to take a longer time than expected to see a noticeable turn. Starbucks is trading at nearly 40x forward earnings and the best long-term options probably still include more downsizing. When you're running a 40,000-unit chain trying to undo years of damage and America's fickle tastes the there needs to be more of a plan than friendlier baristas to keep investors interested.

Starbucks is trading at 2019 levels and is still at least 38x forward earnings. With a turnaround at least another quarter or two away and the stock ramping into next week's report this looks like a great time to declare a (very) small victory on the investment and look for better opportunities.